Floridians who purchase health insurance themselves pay premiums that are about five percent higher than the national average.

Why?

One reason is the Affordable Care Act, or ObamaCare. In Florida, individual‐market premiums have risen an average 12% per year since the law took effect, which means they are now more than double what they were before the law took effect. In fact, premiums are so high, Congress is giving some households earning $212,000 per year a $12,000 government subsidy to help them afford ObamaCare plans.

But that’s not all. As premiums have risen, ObamaCare has made coverage worse for the sick. The law’s supposed “consumer protections” push insurers to adopt narrow networks and other restrictions that ration care for the sick.

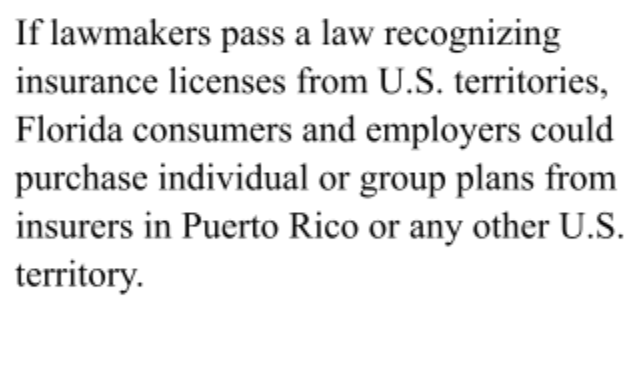

If lawmakers pass a law recognizing insurance licenses from U.S. territories, Florida consumers and employers could purchase individual or group plans from insurers in Puerto Rico or any other U.S. territory.

State lawmakers have it in their power to let Floridians access better, more affordable, and more secure health insurance by opening the state to competition from insurers in Puerto Rico and other U.S. territories.

How?

ObamaCare’s “guaranteed availability, community rating, single risk pool, rate review, medical loss ratio and essential health benefits” regulations are the law’s costliest hidden taxes. They are the main drivers of rising premiums and care rationing.

In 2014, however, the Obama administration exempted health insurance in American Samoa, Guam, the Northern Marianas Islands, Puerto Rico and the U.S. Virgin Islands from those regulations. Subsequent administrations have preserved this exemption.

Many established health insurers already do business in the territories, including Aetna, UnitedHealthcare, Humana y BlueCross BlueShield, — each of which already has provider networks in Florida.

Opening Florida’s market would improve the quality and cost of health insurance. Floridians could save 50% or more on their plans.

Florida employers could offer more flexible and affordable coverage options and compensation packages, including higher wages.

Opening Florida’s market would provide a much‐needed dose of competition. Federal and state regulations create so many barriers to competition that in 2019, just two insurers controlled 92% of Florida’s individual health insurance market.

It would also help struggling territories. Allowing insurers in Puerto Rico (population: 3 million), Guam (153,836), and the U.S. Virgin Islands (87,146) to compete in a market as vast as Florida’s (population: 22 million) could create an economic boom in those territories.

To protect consumers, Florida lawmakers could require disclosures to ensure consumers know what they’re getting. They could further provide that each territory’s health insurance regulations become part of any insurance contract, so Florida residents could enforce consumer protections in Florida courts.

In 2020, Florida opened the state to competition from businesses and professions with licenses from other states. That law is helping restore the rights of workers to earn a living and of consumers to choose whom they patronize.

People have rights when it comes to their health care, too. Just as Florida residents have a right to choose their health insurance, including the right travel to a U.S. territory and buy health insurance there, they have the right to buy those same health plans without leaving home.

Florida law recognizes many occupational licenses from other states. Recognizing insurance licenses from U.S. territories would give Floridians additional choices alongside ObamaCare.

This article was published originally in CATO Institute

1 Carpenter, D. (2021). El derecho de nacimiento de la libertad económica. Instituto de Libertad Económica para Puerto Rico. https://institutodelibertadeconomica.org/wp-content/uploads/2022/01/Article_The-Birthright-of-Economic-Liberty.pdf

2 Stansel, D., Torra, J., & McMahon, F. (2019). Economic freedom of North America 2019. Fraser Institute.